BY DR. TANAI CHARINSARN

APRIL 7, 2017

“The greater danger for most of us isn’t that our aim is too high and we miss it, but that it is too low and we reach it.” — Michelangelo

The concept of setting "objectives" to drive strategy emerged several decades ago, which popularized the idea of Management by Objectives (MBO). This concept teaches that organizations can be effectively managed by "setting objectives" and having everyone figure out the "how" to achieve those objectives. Under this approach, it is believed that if everyone achieves their individual objectives, the organization, as a whole, will achieve its goals. This concept was initially useful at a certain level and eventually gave rise to what is now called Key Performance Indicators (KPIs).

However, what often happens in reality is that organizations employ this concept to set individual goals and let various departments or units develop their strategies to achieve these goals. Often, these sub-strategies don't lead to overall success because they're not well-coordinated. Different units may not collaborate, and work doesn't proceed as planned, ultimately resulting in a lack of success.

Another issue is that when each unit is tasked with developing its strategy, the strategies may not align, leading to conflicting goals. For example, the sales department might want to increase sales by introducing new products or flavors, while the manufacturing department has a goal to reduce costs by decreasing the number of product variants. These mismatches can lead to internal conflicts, hampering the organization's overall performance.

In reality, successful strategy implementation should start with discussions about what needs to be done to make the organization successful in a highly competitive market. Once a comprehensive strategy is developed, objectives are derived from it. Goals are not determined by desired outcomes but are based on the assumption that if the organization follows its strategic plan, "the results should be this way."

The process of goal-setting is intricate because goals serve as motivational factors for individuals, affecting their job performance. Therefore, setting goals shouldn't be a matter of merely assigning numbers to be met. Instead, it should involve the use of financial models to calculate the financial impact of the intended strategic actions. In some cases, sensitivity analysis or scenario analysis may be used to enhance precision.

So, how many goals should be set? The appropriate number of goals is highly context-dependent. They should be specific and realistic, able to be explained using financial models, and receive consensus and buy-in from all relevant parties.

It's worth noting that setting goals too low can lead to complacency, while setting them too high without a well-defined strategy can lead to unrealistic expectations, pressure, and an exodus of talented employees. The most appropriate goals are those that align with the strategic plan, are realistic, and foster collaboration and commitment among all stakeholders.

BY DR. TANAI CHARINSARN

MARCH 2, 2017

“You cannot be everything to everyone. If you decide to go north, you cannot go south at the same time.”— Jeroen De Flander

Many businesses are facing challenges, and executives are reviewing their own operations. Some businesses are at a saturation point where growth is slow or may have stopped. The next question is, what should be done from here? Which direction should the business move forward in? Some may choose to invest in other industries, while others may opt to expand into related businesses. Some still need to address the issues with their existing business to improve performance. Some may need to reposition the business to ensure its continued success. Regardless of the business's current situation, strategic organizational direction remains crucial in assessing the business landscape. Therefore, the question is, what should be reviewed to develop a strategy that leads to the intended success? The following three points need to be considered:

First point: Where Should You Focus?

One business cannot be everything to everyone due to limited resources. Therefore, it is crucial for an organization to choose where it wants to be, what it wants to be, what it wants to offer, and which customer group it wants to serve. You must assess the overall market and the industry, identifying what is missing in the market, what opportunities exist, and what trends may shape the future. The most important question that an organization should answer is, "Why will customers buy our products or services?" As mentioned above, with limited time and resources, organizations need to quickly find the positioning they should focus on in their business. In this day and age, businesses cannot afford to wait; if we don't act, someone else will. Part of the competition depends on timing—those who act first often gain a competitive advantage.

The process of selecting a position has three subcriteria as follows:

-

Uniqueness: The position must be distinctive, meaning it should be a position that no one else currently occupies or one that might be in demand in the future. For example, Starbucks positioned itself as a "third place," different from traditional coffee shops. Initially, people used Starbucks for business meetings, customer interactions, and as a place for students to study or read. However, in recent years, more individuals use Starbucks for quiet, solo work. Entrepreneurs and freelancers are among the customers who see Starbucks as their go-to workspace. While other coffee shops have also started offering conveniences like power outlets and Wi-Fi, none have achieved the same level of success as Starbucks.

-

Alignment with Organizational Capability: The organization should have the capability to deliver on the promises made to customers. If an organization communicates certain commitments to customers, it must be capable of delivering on those promises. Failure to do so means that the organization does not truly own the position. A successful example is Dusit Thani, which is not just one of the luxury hotels, but also a symbol of world-class Thai hospitality and culture. Dusit Thani manages not only its own hotels but also those of others, especially internationally. Additionally, Dusit Thani is involved in various related businesses, such as spas, cooking schools, and hotel management colleges. Currently, Dusit Thani operates many hotel businesses in various countries, including the United States, India, China, Maldives, and the Philippines.

-

Profitability: Ultimately, every business must be able to generate revenue to sustain itself. When choosing a focus, organizations should not overlook the financial aspect. Preliminary research should be conducted to determine how the business can generate income from the selected customer group and business model. The business model may vary in certain industries. For instance, the car rental industry may not seem attractive at first glance due to a relatively limited customer base, often consisting of lower-income individuals, and the higher cost compared to public transportation. However, market growth is favorable as more international travelers come to Thailand. Flight numbers, both domestic and international, are on the rise. Overall, people are willing to pay a premium for convenience, privacy, and the ability to control their own transportation. At the same time, the industry can generate income through various avenues, such as offering GPS rentals, chauffeur services, and fuel tank refills, which can be considered additional revenue streams.

Second point: How to win in the long run?

If the organization chooses the right position and is profitable, other players will soon follow. The next question is, how can a business compete and win in the long run? This is a question that should be addressed early on rather than waiting for declining results or for competitors to catch up. To succeed in the competitive market (the "red ocean"), a business must establish a competitive advantage. This can be achieved through two main strategies: increasing customer willingness to pay and reducing costs.

-

Increasing Willingness to Pay: This strategy involves making the business more desirable to customers, increasing the benefits and value provided to them. It requires continuously understanding customer needs and staying ahead of customer demands by developing products and services that cater to their changing preferences. Organizations need to adopt a consumer-centric approach and be responsive to external factors that influence customer needs. For example, Apple stores in the United States have transformed into community hubs, offering free Wi-Fi, workspaces, and hosting weekly concerts. These changes are aimed at creating an experiential atmosphere and inspiring visitors. Additionally, Apple has expanded its target customer base to include businesses and has designed "Boardroom" spaces for corporate customers to consult with Apple teams on business strategies using Apple platforms.

-

Cost Reduction: While increasing willingness to pay is valuable, it can be imitated by competitors, and customer reactions may not always align with expectations. Thus, cost reduction is a more controllable approach. Reducing costs should never be overlooked, even if the business is already profitable, as it can further enhance profitability. The additional profits from cost reduction can be reinvested into the business to improve its competitive edge. For example, Amazon initially outsourced its shipping operations to third parties, despite the high costs. However, over time, Amazon acquired the capabilities to manage its shipping in-house, especially in areas with a high concentration of customers or near its warehouses. More recently, Amazon has also explored using drones for delivery to cut down on labor and fuel costs. Additionally, Amazon uses its own solar energy farms to produce electricity, reducing the cost of drone operations.

In summary, to achieve long-term success, organizations should focus on creating a distinctive position, enhancing customer value, reducing costs, and continually adapting to changing customer needs and market dynamics. These strategies can help organizations build a strong competitive advantage and thrive in the long run.

Third point: How to proceed and what to learn?

After deliberation and decision-making about where to focus and how to win the competition, the next step is to put into practice what has been planned and written. Taking action is a crucial step to understand whether the planned strategies align with reality. In addition to being a step in actual implementation, it is also a learning process used for further refinement and development of the strategy.

The process of practical implementation includes four main steps: planning, execution, monitoring, and learning.

Planning: In this stage, the organization takes the first two initial questions about positioning and competitive advantage and summarizes them into an action plan. This plan should be as realistic as possible, something that can be executed by the workforce, including clear indicators and responsibilities. It should also be an intelligent plan, which means it uses minimal resources, gets things done quickly, and doesn't involve ongoing, never-ending tasks. This ensures that the organization can realistically execute the plan.

Execution: Execution here does not merely refer to carrying out tasks but involves actively engaging and participating in the activities that make things happen. The workforce will inevitably encounter new problems and challenges, which require precise and decisive decision-making. Successful execution is not possible unless the entire team and management participate fully in the new activities the organization is undertaking.

Monitoring and Tracking: Two things organizations must constantly observe and track are results and assumptions. It is necessary to check whether the results align with the plan and whether the initial assumptions still hold. Many organizations focus on the results. When results don't match the plan, they may believe that the strategy is failing and halt their operations without revisiting the various assumptions and attempting to align them with reality.

Learning: In most cases, true learning occurs as a result of practical implementation. After monitoring results, the next step is to hold regular meetings to update the project's progress. Team members share what they've learned during execution and how that learning can be used to refine or even change the strategy.

The outcome of monitoring, tracking, and learning in results that are close to the Agile implementation method. This method fosters a disciplined approach to project management, promotes continuous examination and adjustment, encourages teamwork and shared responsibility, and develops products or services that genuinely meet customer needs without conflicting with the organization's goals. An example of this is Commerce Bank, which introduced the concept of 'retailtainment' in its bank branches to improve the customer experience and increase customer satisfaction. However, they encountered various challenges during execution, such as inconsistent branch standards and increased expenses without increased revenue. They learned that excitement about new things doesn't always equal customer satisfaction and ultimately abandoned the initial plan.

When all four processes (planning, execution, monitoring, and learning) are combined, managers will have a much clearer direction for the business. They will have a well-supported strategic plan along with operational plans that employees can execute. The success of the set goals will not be too far out of reach. However, the most crucial aspect is defining where the business will focus. It's important to remember that your business cannot be everything to everyone, and simultaneously, managers need to consider the organization's capabilities and whether they align with the organization's goals.

Managers should evaluate whether the workforce has the ability to execute the strategic plan and achieve the set goals. If there are gaps in capabilities within the organization, they need to find ways to address them, whether through employee training or hiring new staff. If the organization lacks the required capabilities, the execution of the action plan in step three will not be efficient, leading to results that do not align with the predetermined objectives.

BY DR. TANAI CHARINSARN

FEBRUARY 16, 2017

“Building a visionary company requires one percent vision and 99 percent alignment.”— Jim Collins

Today, "strategy" is a major focus for every organization everywhere, as they have come to realize that without a strategy, surviving in the business world becomes more challenging. Past strategies, even if successful, do not necessarily apply to the future. In the era of globalization, changes occur constantly and faster than before. This includes changes in market conditions, consumer demands, industry regulations, and technological advancements. Every industry has the potential to be disrupted by smaller players like startups that leverage the internet and technology to introduce new offerings to customers. Traditional business models and limitations are being bypassed. For example, hotels are not just competing with each other but are also contending with platforms like Airbnb. Even banks need to keep an eye on new fintech developments, and the insurance industry is witnessing a surge in insurtech both internationally and, even though less familiar, in Thailand.

Crafting strategies in a VUCA (Volatile, Uncertain, Complex, and Ambiguous) environment:

Developing strategies in a VUCA environment (characterized by volatility, uncertainty, complexity, and ambiguity) is not an easy task. It particularly challenges mindset and internal alignment within an organization. Shaping the mindset of employees is essential to make them believe in and actively participate in the direction the organization is taking. Achieving alignment within the organization is also crucial.

How an organization's capabilities should be in a VUCA environment:

1. Strategy and capabilities should align.

The first question an organization must ask itself is what capabilities are necessary to drive the strategy that the organization currently lacks. To do this, it's important to first identify the existing capabilities and the required capabilities to identify the gaps and figure out how to fill those gaps.

Example of misalignment between strategy and capabilities:

The online grocery business was growing rapidly and seemed promising for the future. Even consulting giant Accenture invested hundreds of millions of dollars in creating an online grocery business named Webvan. Customers could order groceries online and have them delivered to their doorstep. However, Accenture's venture failed within 18 months because the company's capabilities did not align with the chosen strategy. Apart from having no prior experience or knowledge in the supermarket business, their online capabilities required significant development, such as website design, online customer acquisition, and suitable transportation for groceries.

Example of alignment between strategy and capabilities:

At the same time, a giant company like Amazon has similar intentions. However, it is evident that Amazon has a clear advantage when it comes to online capabilities and already possesses a database of online users. Furthermore, Amazon has the capability to handle its own deliveries in multiple cities, with faster delivery times and cost-effective management.

Another example of an organization that aligned its capabilities with its strategy is Tesla Motors. The trend in electric cars is the future of the automotive industry, which uses batteries as a power source. Tesla Motors joined hands with partners to build gigafactories for the production of batteries specifically for Tesla cars.

2. Strategy and capabilities must be agile.

In a VUCA environment, strategies should not remain static because the VUCA environment has become the new normal. Holding onto a single long-term strategy without adapting to the evolving environment is difficult and often leads to failure. Capabilities built to execute past strategies may not be beneficial in the future and may eventually become a heavy cost burden for the organization.

Consumer behavior in the past:

For example, in the banking industry, there was a time when banks everywhere were rapidly expanding their branches to accommodate growth. They were leasing or purchasing spaces to establish branches, hiring more branch employees, and providing training to enhance the knowledge and skills of branch staff, such as sales skills and knowledge of banking products.

Consumer behavior changes today:

However, as people became more accustomed to using the internet and with the growth of smartphones, consumers started shifting towards conducting transactions online rather than visiting branches, as it was more convenient. Consequently, fewer people visited physical branches. This shift led to a surplus of branch employees.

Impact of the VUCA environment:

Many banks had to close certain branches due to them becoming cost burdens on the banks. Additionally, the skills and capabilities of branch staff needed to be developed as traditional sales and product knowledge were no longer as effective. Differentiating and retaining customers within the bank became a matter of managing the relationships with customers that branch employees should possess. In the case of the banking business, the organization's capabilities had to be highly adaptable to respond to these changes, both in terms of personnel and other assets.

Examples of agile strategies and capabilities:

Today, many businesses are shifting towards "renting" resources rather than "buying." This approach provides greater flexibility to organizations, as seen in the growing trend of contracting services rather than hiring full-time employees. For instance, many organizations are now opting to purchase IT management systems as a service instead of owning and maintaining them. Retail businesses, like convenience stores or restaurants, are increasingly focusing on franchise operations rather than growing independently. Numerous startups exhibit high agility and flexibility, making them capable of adapting, changing, or developing their abilities and resources quickly and easily.

Examples of organizations with future-oriented strategies and capabilities:

For instance, Amazon invested in drones as a tool for a new form of delivery that the organization believed would result in faster and more cost-effective deliveries compared to current land-based transport methods. The capabilities of the organization extend beyond just assets and technology; they also involve the capabilities of the employees. For example, when recruiting employees, organizations should consider the potential candidates' suitability for the organization's future needs. Apple, for example, began hiring personnel from the automotive industry to help develop the Apple Car because they believe that transportation and vehicles will be of greater importance to consumers in the future.

Why considering strategies and capabilities is crucial in a VUCA environment:

Having a well-crafted and aesthetically pleasing strategy is one aspect, and having the capability to execute it is another. Many organizations fail to execute their strategies because they lack the capability to drive them. Conversely, some organizations, despite their strategic planning, fail due to a lack of flexible and adaptable capabilities. The world is rapidly changing, and businesses need to adjust and respond to changes to survive. Therefore, organizations must ensure that their strategies and capabilities are aligned, flexible, and future-oriented.

BY DR. TANAI CHARINSARN

FEBRUARY 02, 2017

“Excellence is a continuous process and not an accident.” — A.P.J. Abdul Kalam

If we are talking about the factors that contribute to business success, many people might be able to explain these on the surface. However, when we delve into the specifics of each business and its journey, businesses that achieve success can generally be divided into two major groups.

The first group consists of businesses that achieve success by chance or from seizing opportunities at the right time. These are often the result of doing something right at the right moment. The second group comprises businesses that succeed due to excellent planning, precision, clear strategies, and having capable personnel.

Factors that lead to business success:

The success of a business is typically attributed to two main factors. The first factor is serendipity, meaning doing something right at the right time, and having more opportunities to succeed. For example, BlackBerry initially held a tight grip on the business for several years. They experimented and tried different approaches, and people did not recognize them much. If you mentioned BlackBerry during that time, people might associate it with something like fruit.

However, their management observed the growth of web-based email and mobile phones and decided to study and develop technology that would allow people to send emails regardless of their location. Certainly, these trends were not exclusive to BlackBerry; competitors and other players in the market were aware of the growing trends. Still, BlackBerry managed to combine these two trends at the right time, making people recognize BlackBerry as a brand for mobile phones that could efficiently send emails, offering convenience, ease of use, and security.

Making a business truly successful:

However, it's well-known that success achieved due to luck is often short-lived. The environment and consumer needs change over time. Competing strategies and advantages must adapt to these changes. Therefore, what genuinely makes a business succeed in the long run comes from the capabilities within the organization itself.

Many organizations believe that skills and abilities are the key factors directly affecting business performance and contributing to long-term success. Hence, it's not surprising that many organizations continually conduct seminars, training, and coaching sessions for their employees and executives. They also invest in acquiring individuals with valuable skills from external sources, even if it comes at a high cost. However, the "ability" that truly leads to sustainable business success should not be inflexible. The ability an organization should possess is one that is flexible and dynamic enough to adapt to environmental changes. When strategies change, the ability to perform or operate must also adapt. Therefore, in some cases, developing skills or specific abilities in employees might put the organization at risk, regardless of whether the business operates in an industry with high or low dynamism.

"Dynamic Capability" is the Key

Hence, the concept of "Dynamic Capability" has been introduced, which is a new paradigm for achieving competitive advantage. Dynamic capability refers to an organization's ability to "create, extend, or modify" its resources effectively to respond to the changing environment.

-

Creating Innovation "The ability to create innovation" is often seen in the research and development departments of organizations. Their role is to study, research, and learn from the organization's resources, whether it's knowledge, products, processes, or assets. They then use this knowledge and understanding to create new things that bring benefits, such as new innovations or improvements to existing products. For example, Coca-Cola, or the Coke beverage, is an interesting case study. A few years ago, Coke collaborated with Leo Burnett Colombia to study and develop a non-electric cooling box. After a year of research and development, Coke tested the biological cooling box in Aipir, known to be one of the hottest cities in Colombia. The cooling box operates like a coin-operated refrigerator, capable of storing drinks in three different heights. This innovation not only provides a convenient solution but also extends Coke's reach to a new group of consumers.

-

Expanding Resources "The ability to expand resources" is more broadly visible. It involves expanding into new businesses while building on existing resources. A giant like Google is an excellent example. Google started as a search engine and expanded into various other businesses based on its vast user data. Google now encompasses advertising, email services, and cloud office, to name a few. Another example is Fujifilm, known for photography and cameras. They expanded into producing beauty-enhancing products, such as skincare, makeup, supplements, and beverages. Fujifilm developed nanotechnology and anti-oxidation technology to protect against UV rays and color fading. Under the same concept, they introduced Astalift, a skincare brand that protects against UV rays and boosts collagen production. Recently, Fujifilm partnered with the Kirin beverage brand in Japan to introduce Kirin Astalift Water, a non-alcoholic beverage with collagen and astaxanthin.

-

Modifying Resources "The ability to modify resources" refers to the capability to change or increase the value of existing resources. This process is widespread in competitive industries, where companies differentiate themselves from the competition. For instance, in the highly competitive tea market, where many companies offer similar products, the ability to modify their offerings sets them apart. This may involve changing the aroma, flavor, or appearance of the product to attract consumers and justify higher prices. This value addition allows companies to stand out in the constant pricing war and gain a competitive edge. Therefore, adding value to existing resources is one way to adapt and succeed.

Summary for Organizations with "Dynamic Capabilities"

Dynamic capabilities bring various benefits to organizations. They enable innovation, help organizations revisit and improve existing resources, and identify new business avenues or market opportunities from existing resources. For example, Fujifilm faced a changing competitive environment with increased foreign competitors and digital technology disruptions in the film and photography industry. They responded by reevaluating their strengths and existing resources, starting research and development from their old nanotechnology, and eventually branching out into entirely new industries.

Therefore, organizations with dynamic capabilities need to strike a balance between stability and the ability to adapt continually. This means having the stability to consistently deliver value to customers while being flexible enough to adjust when necessary. Dynamic capabilities must be robust enough to provide continuous value in their unique form to customers, while also being flexible enough to adapt when required.

BY DR. TANAI CHARINSARN

JANUARY 20, 2017

“Action is the foundational key to all success.” — Pablo Picasso

Over the past few decades, strategists have been searching for the answer to what makes a business more successful than others, and two prominent concepts emerged: "positioning" in the hearts of customers and "possession" of valuable resources. However, in recent times, strategic thinking has shifted its focus towards "entrepreneurial execution," a theory driven by a visionary perspective.

In the 1980s, the widely accepted concept was "positioning," where strategists believed that occupying a unique and distinctive place in customers' minds would make them memorable and perceived as offering more value than competitors. This notion still holds significant importance in contemporary business, especially in branding and marketing, as it cultivates brand loyalty and a willingness among customers to pay a premium for a perceived superior value.

Business Examples Illustrating the "Positioning in Customers' Hearts" Concept:

-

Walmart: Walmart's clear positioning as "Everyday Low Prices" has made it synonymous with affordable shopping. Customers looking for budget-friendly products often think of Walmart first, creating a strong competitive advantage for the company.

-

MINI Cooper: The MINI Cooper, despite being a premium car, positions itself as a fun and youthful choice, appealing to a demographic seeking an exciting driving experience. This demonstrates that positioning isn't limited to a specific age group or income level, but rather about creating a distinct place in customers' hearts.

The Concept Acknowledged in the 1990s: "Possessing Valuable Resources"

In the 1990s, strategic thinking shifted to focus more on an organization's internal factors. Strategists began to evaluate a company's resources, skills, abilities, strengths, and areas of expertise. The idea revolved around the belief that a successful business was one that possessed superior resources or competencies compared to its competitors, such as having cost-efficient supply chains or highly skilled personnel.

Business Examples Illustrating the "Possessing Valuable Resources" Concept:

-

Fast-Food Chains: Companies like McDonald's and 7-Eleven have excelled in the fast-food and convenience store industries, respectively, partly due to their advantageous physical locations. These prime locations ensure high foot traffic, which is crucial for their success. As a former McDonald's CFO once said, "We are not in the food business; we are in the real estate business."

-

Technology Companies: In the tech industry, companies that invest in research and development and have superior technological capabilities often lead the market. For instance, companies like Apple, Samsung, and Huawei have maintained their competitiveness through innovative products and technology.

The Current Acknowledged Concept: "Entrepreneurial Execution"

In contemporary times, strategic thinking is increasingly focused on "entrepreneurial execution," where new or smaller companies compete with industry leaders by offering innovative and disruptive products or services. These companies may identify niche market segments or fulfill under-served consumer needs that larger corporations may overlook. The success of these new entrants doesn't necessarily stem from having more resources or superior technology but from understanding consumer preferences and having the courage to innovate and fill gaps in the market.

Business Examples Demonstrating "Entrepreneurial Execution":

-

Innovative Startups: Small startups that introduce disruptive innovations or cater to niche markets often succeed by educating consumers about their new products or services. They may redefine customer preferences and change their customers' loyalties.

-

Small Companies Competing with Industry Giants: Smaller companies may compete effectively with industry giants, not because they have more resources or better technology, but because they understand consumer needs and take calculated risks by introducing innovations or filling market gaps.

This shift in strategic thinking highlights the importance of entrepreneurial spirit, adaptability, and understanding customer behavior in the rapidly changing business landscape.

Business Examples Demonstrating "Positioning in Customers' Hearts" Concept include Facebook, Airbnb, Uber, and "Tao Kae Noi."

Recent strategic thinking has emphasized having a vision and entrepreneurial execution. This means taking risks, getting hands-on, and being agile in business operations.

In conclusion, while strategic concepts evolve with time, there is no one-size-fits-all theory for success. Success is often a result of various factors coming together, combining excellent resource possession with the courage to take action. Some businesses can indeed secure a position in customers' hearts, but they must also deliver on their promises to maintain long-term success. Similarly, start-ups and newly emerged businesses must do more than just being bold and visionary; they need strategic thinking, comprehensive planning, and adaptable resource management. Having the best resources doesn't guarantee sustainability, as resources eventually deplete. Machinery will become obsolete, employees retire, and so on. Therefore, the answer to the question of what makes a business successful remains ever-evolving and requires continuous study and the development of concepts according to the era.

BY DR. TANAI CHARINSARN

DECEMBER 18, 2016

“Until you cross the bridge of your insecurities, you can’t begin to explore your possibilities.”—Tim Fargo

The term "Diversify" can be applied at both the organizational and personal levels, but it is mostly used in the context of diversifying business and investment risks. In this article, diversification doesn't only refer to risk diversification but also expanding into new directions and choosing new paths for organizational growth.

Many businesses that have been thriving often exhibit "Concentric growth," which means they grow by offering variations of existing products and services to their existing customer base. For example, a company might offer the same product to the same group of customers but with changes like different flavors or packaging. This approach is chosen by many organizations because it is relatively easy and carries less risk. It's often referred to as staying within their "comfort zone" where they have an advantage and experience.

Simultaneously, rapid technological advancements and changing consumer behaviors have led to increased competition in both existing and new markets. Product lifecycles are getting shorter, and sticking with the same old products and services might lead to risks. Therefore, diversification, or expanding into new markets or products, becomes essential.

Diversification involves addressing the following three key questions:

-

Choosing the Industry: Before expanding the portfolio into a particular industry, you need to consider external factors. These factors may include future trends, profitability in that industry, and past growth rates.

-

Mode of Entry: Deciding how to enter the industry is essential. This can involve various strategies, including importing and exporting, making contractual agreements (e.g., franchising and licensing), or investing through joint ventures or starting a new business. In most cases, organizations tend to expand their portfolio through multiple entry strategies.

-

Competitive Advantage: To succeed in a new industry, it's crucial to have a competitive advantage. This can be achieved in three main ways: a. Differentiation: Creating a unique product or service that stands out from competitors. b. Low-Cost Advantage: Offering products or services at the lowest price in the market. c. System Lock-In: Becoming a market leader, setting industry standards, and making it difficult for competitors to replace you.

Diversification can also apply at the personal level. Individuals need to plan their careers and futures, just as organizations do. You have to consider which industry you want to enter, whether you should start your own venture or work for an existing organization, and how to gain a competitive edge in your field. Gaining certifications, licenses, or additional qualifications can set you apart from others.

In summary, diversification is a strategy that organizations and individuals use to reduce risk and explore new opportunities in various industries. The key is to make informed decisions about which industry to enter, how to enter, and how to gain a competitive advantage.

BY DR. TANAI CHARINSARN

NOVEMBER 28, 2016

“It is not the strongest or the most intelligent who will survive but those who can best manage change.”—Leon C. Megginson

A long time ago, nature taught us one rule, which many of you may have heard of - the rule of "Survival of the fittest," or the survival of the most suitable, as described in Charles Darwin's theory of evolution. However, in every era, the fittest are those who can adapt to changes in their environment, rather than necessarily the strongest, the most resilient, or the most intelligent. This concept also applies to those who thrive in different economic eras, from the Agricultural Economy to the Global Economy and the Knowledge Economy.

In today's rapidly changing environment, both traditional competitors and new market entrants often have the same goal - to compete for market share and capture the hearts of consumers. Adhering to traditional business models might not make one the fittest anymore.

So, how can adaptability be a competitive advantage?

Regarding adaptability, many people still think of it as reacting to change. However, waiting for the environment to change before adapting may not be timely. In this era, businesses need to be sensitive to the early signs of change, even if they are faint and not yet clear. We are talking about "proactive adaptation" rather than just reacting.

Three continuous factors that businesses should observe and monitor are consumer behavior, technology, and global connectivity:

1) Consumer Behavior: Studying the economic history reveals that consumer desires are a significant driving force behind economic changes. Initially, people's needs were basic, such as having enough food and shelter. As producers met these basic needs, people began seeking convenience, industrial products like cars or phones, and various services like restaurants, beauty salons, hotels, and healthcare.

As consumer needs evolve in the hierarchy of needs, businesses must adapt and offer more than just functional and emotional fulfillment. In the present era, consumer identity and value play essential roles. People buy products that reflect their identity, making customization a part of their value. Identifying these changes and seizing the opportunity to meet new consumer desires is crucial.

2) Technology: Technology is advancing rapidly in our current era, offering businesses the chance to operate more efficiently and cost-effectively. New generations are open to adopting the latest technology and are more willing to experiment. Consequently, the speed at which change occurs has increased due to the shortened technology adoption and product life cycles.

Therefore, monitoring and keeping up-to-date with technological advancements are crucial. This includes not only technology within your industry but also innovations from other industries that can be applied to your business.

For example, businesses in the food industry have started using tablet devices as menus, allowing customers to order directly from their tables without the need for a server. This is just one example of how technology from the information and communication technology industry has been applied to the service industry.

3) Global Connectivity: In this era, businesses can't operate in isolation. Open trade, rapid cross-border transportation, and the emergence of low-cost airlines have made global travel accessible to everyone. The internet connects customers and producers worldwide, expanding opportunities and markets. The food industry in a city like Bangkok doesn't cater solely to local customers but also to international tourists. This interconnectedness enables businesses to reach new customers and expand their reach.

Businesses need to look at both the supply and demand chains and continually observe and adapt to changes. They should assess factors that could affect their industry and seize opportunities or mitigate risks, such as the potential for establishing low-cost production in another country.

In summary, adaptability is a vital trait for businesses in the modern era, and it is achieved by staying attuned to changes in consumer behavior, technological advancements, and global connectivity. By proactively adapting to these factors, businesses can secure their competitive edge and thrive in an ever-evolving environment.

BY DR. TANAI CHARINSARN

NOVEMBER 05, 2016

“If you do not seek out allies and helpers, then you will be isolated and weak.”—Sun Tzu, “The Art of War”

Whether in the world of business, sports, or any competitive game with more than one player, everyone always thinks of competing for victory. Whoever has an advantage wins. However, the age of such advantages is getting shorter every day, and the number of players is increasing, especially sub-players.

Meeting consumer needs in the past In the past, those who could meet the needs of consumers and had high production capacity often dominated the market. However, over time, more players began to see the business opportunity in focusing on emotional needs, even if the products were similar. If they had a better design, looked better, or were more appealing, they could capture customers from the traditional market leaders. This is even more evident in the current era, where information sharing can be done globally, and accessing low-cost manufacturing facilities in other countries is not difficult. Competition in terms of product specifications and production capacity can no longer create a competitive advantage. Many businesses in the same industry face intense competition, resulting in lower revenue and profit.

Evolution of Strategies to Meet Consumer Needs Therefore, the idea of collaboration emerged as a replacement, creating partnerships (Alliances) to generate new, unique values for consumers. Collaboration can occur at various levels, from joint campaigns and cooperation agreements to joint ventures or even mergers and acquisitions. However, it is essential to consider that not all collaborations are successful. Often, conflicts arise between both companies, leading to their eventual separation. Based on the study of such cases, three key success factors for collaboration have been identified.

-

Organizations Must Have Different Positioning or Value Propositions Both organizations must have different positioning or value propositions because if they offer the same value proposition and target the same audience in the same market, collaboration may not be as effective as when they have different value propositions. A difference in positioning or value proposition allows the partnership to offer unique value and potentially attract customers from the traditional market leaders. For example, when Honda collaborated with bicycle dealers in different provinces to help sell Honda motorcycles, Honda gained access to showrooms and outlets without the need to invest in creating new ones. Meanwhile, the bicycle dealers earned a higher income through motorcycle sales.

-

Partner Organizations Must Support Each Other's Capabilities The abilities or competitive advantages of partner organizations must complement each other. Collaboration can occur between two companies in the same industry, even when one has a competitive advantage in one aspect, such as product manufacturing or design, while the other excels in distribution or transportation networks. Partnerships between organizations with different abilities can be successful as long as they support each other's collaboration efforts.

-

Compatibility and Cultural Alignment Often, conflicts and disagreements arise when senior management holds different opinions and have incompatible cultural values. It can lead to delays in decision-making or decisions that lack commitment and follow-up. Therefore, collaboration can be successful when there is compatibility and alignment in organizational culture. When both parties share a similar vision, goals, and values, they can successfully drive the collaboration.

In conclusion, to succeed in collaboration and partnership, organizations must have different value propositions, support each other's capabilities, and ensure compatibility in culture and values. These factors are essential for creating and maintaining successful collaborations.

BY DR. TANAI CHARINSARN

OCTOBER 26, 2016

“Without strategy, execution is aimless. Without execution, strategy is useless.”—Morris Chang

The term "Strategic Management" refers to looking into the future and determining the direction in which a business should proceed. It often involves making high-level decisions to bring about significant organizational changes, ultimately aimed at gaining a competitive advantage in the long run. Therefore, strategic management is not just about annual budget planning, goal setting, creating new marketing plans, or introducing new products. Every plan and activity should align with the organization's direction and strategy.

The three essential components necessary for developing a strategy including context, tools, and processes.

- Context

Strategic management relies on context-specific decision-making. There is no one-size-fits-all formula that can be easily studied and replicated. It depends on various contextual factors, both internal and external to the organization, such as its history, culture, and environmental factors. These contextual factors shape an organization's unique characteristics. What works for one business in a particular industry may not work the same way for another business in the same industry.

For instance, the success story of Starbucks, a coffee shop business, has been widely publicized and even taught in universities. However, if a new entrepreneur wants to open their coffee shop and aims for success similar to Starbucks, duplicating Starbucks' strategies may not guarantee the same results.

- Tools

Tools, frameworks, and theories remain essential in strategic management. They help in structuring thoughts and formulating new ideas. While the younger generation might sometimes overlook these theories in favor of practical experience, in reality, theories are equally vital. Success in business cannot rely on luck alone, but it requires knowledge and understanding.

There is a wide array of management tools available, such as SWOT analysis, Five Forces, PESTEL analysis, Value Chain Analysis, Benchmarking, VRIO analysis, among others. These tools help organize thoughts and determine the desired outcomes. It is essential to use these tools correctly and choose the right ones to address the specific problem at hand.

- Processes

Once the context and tools are well understood and results have been achieved, the next step is developing and implementing the processes. It's vital to ensure that everyone in the organization understands the same goals, sees the same picture, and knows where the company is heading.

Creating a shared understanding is essential. Commitment from all team members is crucial as well. Often, things might not go as planned, and it is at this point that commitment becomes vital. Ensuring that people are responsible for their actions and outcomes is a significant part of the process.

Furthermore, managing the changes in direction is part of the process, and often, it requires meticulous planning, clear delegation, and follow-up on whether the agreed processes are being followed. Detailed plans, however, might fall by the wayside due to various challenges, but it is essential to adapt and evolve to ensure long-term success.

In summary, strategic management is a dynamic process that requires a deep understanding of context, the right tools, and an efficient process to achieve desired outcomes and success.

BY DR. TANAI CHARINSARN

OCTOBER 25, 2016

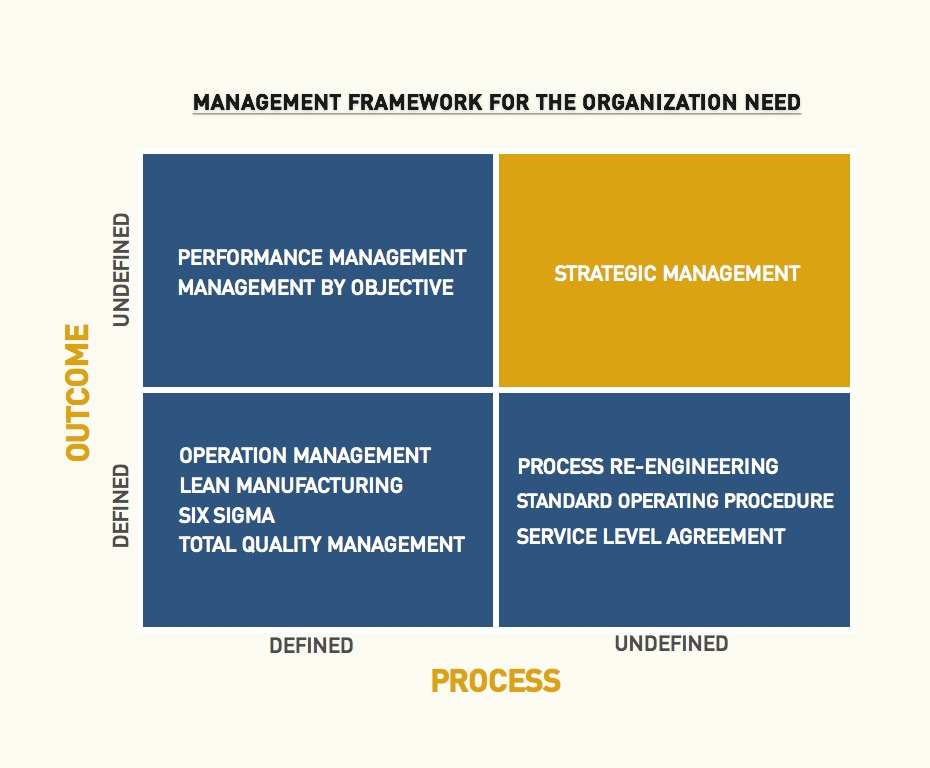

Managing organizations with varying levels of ambiguity can be done in several ways. Typically, each organization tends to choose different strategies. The framework of this article is derived from examining the management concepts of organizations that have different processes and outcomes in their operations, which depend on the nature of each organization.

Defining a management framework suitable for each business type will enable strategists and managers to efficiently choose the tools for managing their organization. They can focus on the essential tools for the organization without wasting time on unnecessary matters, as the business world is constantly evolving and never stands still. Wasting time on unnecessary matters may lead the organization astray and make it difficult to recover.

Management Framework

If we evaluate the characteristics of organizations based on the clarity of their "process" and "results," we can identify four patterns:

-

Organizations with clear work processes and performance measurement: We often observe this type of organization in large industrial manufacturing businesses, such as automobile part production, ready-to-eat food production, and paper manufacturing. These organizations have well-defined work processes and clear performance metrics, such as production quantity per time period, production quality according to standards, or revenue per production cycle. Management concepts suitable for this type of organization include Total Quality Management (TQM), Operation Management, Six Sigma, and Lean Manufacturing, which enhance work process efficiency and lead to desired outcomes. These organizations can track and monitor work results effectively, fostering competitiveness and profitability. Examples include Toyota and CPF Corporation.

-

Organizations with clear work processes but unclear performance measurement: Government systems are a good example of organizations falling into this category. They have well-structured work processes, document formats, and systematic workflow, but they often lack clear criteria for measuring work success. For example, government offices, transportation agencies, and document processing services may have clear processes, but they don't specify measurable outcomes. Management approaches for such organizations include Performance Management and Management by Objectives (MBO), which help employees work toward specific goals. Common tools in this category are Key Performance Indicators (KPIs) and the Balanced Scorecard. Examples include government agencies and banking institutions.

-

Organizations with unclear work processes but clear performance measurement: Small businesses often fall into this category, particularly when the business owners set their goals and outcomes without clearly defined work processes. Without established processes, these organizations cannot confirm their success due to the lack of systematic work. To address this, they need to establish work processes and standards. Management concepts for such organizations include Process Re-engineering, Standard Operating Procedures (SOPs), and Service Level Agreements (SLAs) to control and standardize their work processes and create agreements about the work scopes for each department within the organization. Examples include small and medium-sized enterprises (SMEs).

-

Organizations with unclear work processes and unclear performance measurement: This category typically includes new organizations or those undergoing significant changes in direction and operations. Start-ups and organizations with changing management may need to rely on strategic management concepts to plan and set the direction for their work. This helps unify the organization's vision and goals, even when work processes and outcomes are not yet clear. It's crucial for each organization to understand its current state and the nature of its business to choose the right management tools and ensure effective management within the organization.

Understanding the organization's current situation and having a clear view of its business characteristics allows each organization to choose the appropriate management tools and truly improve organizational management efficiency.

BY DR. TANAI CHARINSARN

SEPTEMBER 15, 2016

WINNING STRATEGY

Who are our business customers?

It is essential for a business to identify its primary customers. Who are the individuals or entities with the authority to pay for our products or services? For instance, a major company like Facebook Co., Ltd., which owns the social network giant Facebook, Inc., is the real customer for their organization. It is not the number of users in their system but rather those who pay for advertising. Having a large user base only provides visibility (Eyeballs) and doesn't guarantee that advertising on Facebook will be effective. Even though the user engagement rates might be high, the Click-Through Rate (CTR) remains relatively low.

Even though Facebook recently announced having over a billion users, they faced challenges in the stock market, and their stock didn't perform as expected. In contrast, giant search engine companies like Google Inc. are popular among high-value investors, and Google continues to benefit significantly from advertising space sales.

The limitation Facebook faces is that its service users don't primarily come to buy products or services. Instead, the real benefit lies in connecting with friends and social communities. This is different from Google, where users come to search for products or services they genuinely need. Users are more interested in making purchases, which results in higher Click-Through Rates (CTR) for advertising on Google. Advertisers have more trust in Google's platform. Additionally, the shift towards mobile device usage instead of desktop computers has affected Facebook's performance, making Google a more favorable choice for displaying ads. These two factors represent significant challenges in building trust among advertisers for Mark Zuckerberg and his team.

What benefits do our customers get from our business?

In terms of strategy, we look for the Value Proposition or the benefits offered by the business. Put simply, if our business didn't exist, would customers be worse off? If not, it means our business isn't providing any real value. Another aspect that strategic analysts must consider is Customer Insight and understanding where the Unique Selling Point (USP) of the business lies. For example, Starbucks Coffee's brand benefits customers by providing "The Third Place." This is due to an observation of changing consumer behaviors. Starbucks Coffee's customers are those who seek a place to work, meet, chat, have a drink, and have a convenient meeting spot, whether they're in groups or alone. Recognizing the value a business delivers to its customers is critical for building an efficient strategy.

How will the business be operated?

Once a business understands what customers need, the crucial element is the business's capability and the resources required to make it a reality (Operating Model). This is vital for a business's competitive capability. It involves preparing all the necessary resources, such as raw materials, personnel, machinery, and equipment, and combining these abilities to deliver value as promised to customers. For instance, Starbucks Coffee focuses on quality control of coffee beans, training baristas, interior store design, and the ambiance, including decor, music, and coffee aroma.

How will the business make money?

The ultimate answer in business is profitability because, without profit, a business will only survive as long as it has capital. Although financial support can be obtained to help keep a business afloat, one must recognize that no one is ready to assist continuously. Even if a business has a delayed profit, it's essential to consider that the business will eventually generate profit. An example of a business that had the ability to make money in the future is Amazon.com, a company that accepted losses for over 10 years. In the end, it managed to generate profit.

The Operating Model that Amazon.com executed effectively involved collecting various types of books worldwide on its website and selling them at lower prices than the market. Customer service, such as allowing hassle-free returns, even if customers were not satisfied, was a crucial part of their strategy.

( For more details : http://www.amazon.com/gp/mpd/permalink/m3RY5SZWBOJZFO/ref=ent_fb_link )

How will we differentiate ourselves from long-term competitors?

The challenge of creating a good strategy is ensuring the business's sustainability and finding ways to make your business unreplicable. Conducting a SWOT analysis of competitors will help assess if they can copy your business. If you have Distinctive Competency and engage in complex activities that are unique and interconnected, it will be difficult for competitors to replicate your business.

Remember, these are essential elements to consider when crafting a business strategy. They will help the business identify its target customers, understand what benefits it provides, define how it operates, and determine how it generates profit and distinguishes itself from the competition.

Sources :

http://www.starbucks.co.nz/index.cfm?contentNodeID=415

http://www.seattlepi.com/business/article/Fair-Trade-coffee-growers-emphasize-quality-1064046.php

http://www.jingdaily.com/to-caffeinate-china-starbucks-takes-a-page-from-burberrys-playbook/9809/

http://www.whatsonxiamen.com/wine_msg.php?titleid=1416

BY DR. TANAI CHARINSARN

August 10, 2016

“ The plan is nothing but planning is everything ” - Dwight D. Eisenhower

STRATEGY PROCESS BY STRATEGIC LEARNING (SENSE & RESPONSE)

STRATEGIC LEARNING

Strategic Learning Cycle

This theory is a combination of both theories in the process of strategy development. To move from learning to a specific strategy, it is necessary to have a feedback loop to continually evaluate and improve what has been done. The integration of both approaches in this process is called the Strategic Learning Cycle.

PHASE 1: DIAGNOSE - Business Diagnosis (2-3 months) During this phase, the business should focus on learning from the outcomes of the previous year's strategies in terms of employee performance, market changes, and competition. It's important to gather extensive data and use that data to gain insights into the business. Various individuals at all levels of the organization should contribute data based on their interactions with customers, supplier satisfaction, and market conditions.

PHASE 2: DESIGN - Business Design (2-3 days) In this phase, the business should design its strategy to create a competitive advantage and foster innovation. This design should be based on the insights gathered from the data. Senior management, using suitable tools like SWOT and 5-Forces analysis, should be responsible for this phase. The outcome is an idea that should be further explored and developed into the next strategic plan.

PHASE 3: BUSINESS VALUE ANALYSIS (ROI) (1-2 months) This step involves creating a business plan to assess the financial viability of the chosen strategy. It includes market feasibility, operational planning, and financial planning. The goal is to evaluate whether the strategy is financially beneficial for the company. It is important to understand that this is not a one-time activity but a process of planning to enhance the business's success by making it more accurate and efficient.

PHASE 4: PILOT SCALE PROJECT (3-4 months) Since it is difficult to predict if the planned strategy will work as intended, this phase involves implementing a pilot-scale project to learn from trial and error. A successful pilot project should be a full-scale, yet small, implementation. Results are assessed after the specified time to learn what works and what doesn't. The goal is to determine whether the strategy should continue at a larger scale and to identify the conditions for its success.

PHASE 5: EXECUTION In the final phase, everyone in the organization must actively participate in executing the strategy. Management takes the lead in facilitating change, and project managers act as change agents. Changes may involve how success is measured, operational processes, organizational culture, employee development, and IT system support for operations. The key is to keep trying and learning through practical implementation until the strategy is precise and successful.

This process combines theoretical and practical aspects and ensures that the strategic plan aligns with the business's potential to compete in the market.